Pace Digitek’s Accounting Optical Illusion hiding Hidden Value, Most Investors Are Missing

Mar 16, 2026

Please read it on substack for better formatting, Link :

Accounting Can Hide Reality: The Pace Digitek Case Study

Accounting captures the true picture for most companies, but for some companies it doesn’t show the full economic reality. In such cases, investors must adjust their interpretation of the numbers.

We have already seen this phenomenon in SaaS companies like TechNVision, where product development costs are expensed instead of being capitalized as assets on the balance sheet. Link .

I first discovered TechNVision when the stock was around ₹20, and today it trades near ₹6,000 — roughly a 400X return. I publicly wrote about it when the price was around ₹45, which still turned out to be about a 130X opportunity.

Link: https://t.co/hrLkCmbjkk

Similarly, I had written about Garden Reach Shipbuilders when it was around ₹110, and today the stock is went to ₹3,500, delivering nearly a 33 times return. (Post Link)

Over the past 10 odd years, only a handful of investors have managed to publicly share ideas that eventually turned into hundred-baggers. I mention this not to look back, but to explain the context of my current thinking. In recent years my portfolio has become more diversified, and it has been difficult to find opportunities that combine high margin of safety, strong conviction, and exposure to a long-term structural decadal growth theme. After a long time, I believe I may have finally found an idea that fits my criteria for publicly sharing, even though doing so always carries the risk of criticism or trolling if the thesis does not work out.

I am a big admirer of Ian Cassel from MicroCap Investing, and one of his principles has strongly influenced my approach: you should understand your high-conviction idea better than anyone else in the market.I followed this principle wholeheartedly in the case of TechNVision. Over the last 10 and a half years, I continuously tracked and shared developments related to the company and its subsidiaries Solix and Emagia. I probably wrote more than 300 tweets discussing different aspects of the business and hidden prospects. The result was extremely rewarding in terms of investment returns—I made around 200–300× on my holdings. However, the downside was that I also lost lot of followers who were not interested in continuously hearing about TechNVision.

In contrast, I did not need to do the same with Garden Reach Shipbuilders, because the story was already quite visible to the market and the stock moved smoothly upward from my buying price without requiring constant discussion.

For this reason, I would request you to read the entire article on Pace Digitek carefully. If the company or the thesis does not interest you, it may be better to unfollow me, because I will definitely be writing many more posts and tweets about its business developments going forward.

Now you might ask: Why am I talking about accounting limitations in the case of Pace Digitek? TechNVision is an enterprise AI SaaS product company it was unique and most misunderstood company, and it is perhaps the only company in this space that expenses all of its product development expenditure directly through the P&L instead of capitalizing it on the balance sheet. In contrast, Pace Digitek operates as an EPC company, and unlike the SaaS sector, there are many EPC companies already listed in the market.

Answer , the same accounting limitations may distort how investors interpret Pace Digitek’s growth and profitability.

The Revenue Confusion: ₹4200 Cr Execution vs ₹3200 Cr Guidance

Pace Digitek currently has an order book of around ₹10,500 crore, and management has indicated that roughly 40% will be executed in FY27.

That implies:

Order execution: ₹4200 crore

Plus additional non-order revenue

Yet the company is guiding only ₹3200 crore revenue. Naturally, the question arises:

Why this discrepancy?

The answer lies in accounting consolidation rules.

The company may execute ₹4200 crore worth of work, but accounting standards will allow them to report only ₹3200 crore, because inter-group transactions must be eliminated in consolidated financial statements.

To understand this clearly, we must examine the structure of the Pace Digitek group.

Pace Digitek Is Not Just an EPC Company

Pace Digitek is not a normal EPC contractor. The company operates with two core capabilities:

EPC execution

Product manufacturing

The manufacturing capability comes from the acquisition of Lineage Power from GE.

This created a structure like this:

Pace Digitek (Parent)

Executes EPC projects

Lineage Power (Subsidiary)

Manufactures products such as BESS components

Why Consolidated Revenue Gets Reduced

Let’s illustrate with a simple example.

Assume:

Pace Digitek executes an EPC project worth ₹1000 crore

The EPC project uses ₹300 crore of products from Lineage Power

Then:

![]()

Total economic activity:

₹1300 crore

However, consolidated accounting requires elimination of inter-company sales.

So the consolidated financials will show:

₹1000 crore revenue

instead of ₹1300 crore.

Profit Is Not Distorted — But Revenue Appears Lower

Interestingly, profit is not affected. Why?

Because:

Pace Digitek records the product purchase as expense

Lineage Power records profit on the product sale

When consolidated:

profits are combined

internal transactions cancel out

So the profit picture remains accurate.But the revenue picture becomes misleading.

Why This Matters For Investors

This accounting treatment creates two problems for investors.

1. Growth Appears Lower

Current numbers:

TTM revenue: ₹2228 crore

Management guidance: ₹3200 crore

This implies 43% growth.

But the economic activity is closer to ₹4200 crore, implying growth closer to 88%.

Even adjusting for base year accounting effects, the real growth could be around 60–70%.

2. P/S Based Valuations Become Distorted

Some investors value companies using Price-to-Sales ratios.

If the sales number itself is structurally understated, then the company may appear more expensive than it actually is.

A Simple Workaround Example

Consider an alternative structure.

If Lineage Power sells products to an unrelated third party (ABC), and ABC sells those products to Pace Digitek:

Then consolidated revenue becomes:

₹1000 + ₹300 = ₹1300 crore

because the transaction is no longer intra-group.

Another Structural Solution: Separate Listing

Another theoretical solution would be: Listing Lineage Power separately.

However:

accounting rules would still eliminate inter-company revenue

but markets would value the companies separately

which could unlock value.

BOO Projects Create an Even Bigger Accounting Illusion

The accounting distortion becomes much larger in BOO projects (Build-Own-Operate).

These projects were not present in the previous base year, meaning they will create a large optical distortion in future reported numbers.

BOO projects involve three revenue layers:

EPC execution

Product manufacturing

Long-term annuity income

If the company executes a BOO project worth ₹X, then total economic revenue during construction may reach 1.6X, followed by annuity income for 12–25 years.

The Three-Layer BOO Structure

From the concall, Pace Digitek intentionally separated the BOO structure into three legal layers.

Pace Digitek (Listed Parent)

EPC execution

Lineage Power

Supplies BESS products

SPVs under TransGreenX Energy

Own the assets

Earn long-term annuity revenue

The Triple Profit Model

This structure allows Pace Digitek to earn three layers of profit.

1️⃣ EPC Margin: 8–10%

2️⃣ Product Margin: 13–15%

3️⃣ BOO Project IRR: ~14%

Management even hinted that real IRR including internal margins could reach ~19–20%.

Understanding the ₹5025 Crore BOO Order Book

Pace Digitek has ₹5025 crore BOO order book.

However, this does not mean only annuity income like other BESS BOO developers such as:

SPML

GPIL

Patanjali

Ddev Plastics

Instead:

The EPC work itself will also be done by Pace Digitek and paid by its own SPVs under TransGreenX Energy.

How the Financing Works

The financing structure typically looks like this:

30% Viability Gap Funding (VGF)

70% Debt + Equity

The SPV can pay Pace Digitek quickly from this financing pool, which also reduces receivable cycle risk.

Economic Revenue From ₹5025 Cr BOO

From a purely economic perspective:

Total economic activity:

≈ ₹13,000 crore ( 8000 revenue + 5000 asset)

Yet consolidated accounting will show:

Zero construction revenue because internal transactions are eliminated.Instead, the financial statements will show:

₹5025 crore asset on the balance sheet.

Economic EBITDA vs Reported EBITDA

Step 1 — The Economic Reality (What Actually Happens)

During the construction phase of the BOO project, Pace Digitek performs two real economic activities:

EPC construction

BESS product manufacturing (60% of EPC as per con call)

EBITDA Generated

Total economic EBITDA generated during construction : ₹870 crore

This value is real cash profit created during the build phase.

Step 4 — What Happens in Consolidated Accounts

Now accounting standards require elimination of inter-company transactions.

Since the SPV belongs to the same group:

EPC revenue from Pace Digitek → SPV

Product revenue from Lineage → SPV

Both are internal transactions.

Therefore they are removed during consolidation.

The Accounting Optical Illusion

What Happens After Commissioning?

Once the BESS project is commissioned: Revenue starts appearing as:

Rental / annuity income over:

12 years for standalone BESS

25 years for solar + BESS

The P&L then includes:

rental income

depreciation

interest

O&M costs

This produces the ~14% equity IRR (Cashflow) mentioned by management.

Why This Matters for Investors

Short-Term Optical Issue

Large BOO order book

but reported revenue appears lower

Long-Term Economic Reality

EPC margins are real

product margins are real

long-term annuity income is real

But accounting hides the upfront economics.

Management Acknowledged the Accounting “Leakage”

Management mentioned possible solutions including:

sale-and-leaseback structures

platform-level monetization

potential future de-merger of TransGreenX

What Happens to Cash Flow During BOO Construction

In a BOO project, the structure is typically:

Pace Digitek (EPC contractor)

Lineage Power (product manufacturer)

TransGreenX SPV (project owner)

The SPV pays for:

EPC work

BESS equipment

But if the SPV is part of the consolidated group, those payments are internal cash transfers.

Inside the group:

Pace Digitek receives EPC payment

Lineage receives product payment

But at group level, cash simply moves from one pocket to another.

Therefore: Consolidated cash flow does not increase from these internal payments.

Why Pace Digitek Should Be Valued Using SOTP Valuation Method

Even today, the market largely values Pace Digitek as a conventional EPC contractor, applying valuation multiples similar to other EPC companies. In a normal market environment, pure EPC businesses typically trade at a P/E band of around 15–20, and the market appears to be using a similar framework to value Pace Digitek.

However, this approach does not fully capture the true nature of the business.

The more appropriate way to value Pace Digitek is through a Sum-of-the-Parts (SOTP) framework, because the company is not merely an EPC contractor. It is a hybrid platform combining EPC capabilities with high-technology power electronics manufacturing. This manufacturing capability is not ordinary industrial production; it requires deep technical expertise in power systems and energy infrastructure.

Pace Digitek possesses this capability largely because of its acquisition of Lineage Power from General Electric (GE). Pace Digitek inherited a strong technology base and engineering capability that differentiates it from traditional EPC companies.

To estimate the intrinsic value of Pace Digitek, it is useful to conceptually break the group into several distinct businesses and assume that each operates as an independently listed entity. Such a structure would make the underlying business segments more transparent and could potentially unlock value. Of course, implementing this structure in reality would introduce additional related-party transactions and compliance overhead, but it would also provide clearer visibility into the economics of each division.

Under this conceptual framework, the Pace Digitek group can be divided into the following entities:

Pace Digitek Holding Ltd – The parent holding company overseeing the group

TransGreenX Energy – The BOO (Build-Own-Operate) platform for energy infrastructure assets

Pace EPC – The engineering, procurement, and construction division

Pace Lineage Power BESS – The first product division focused on battery energy storage systems

Pace Lineage Telecom – The second product division serving telecom power infrastructure

Pace Defense and Aerospace – The third product division targeting defense and aerospace power systems

Pace ICT – The digital infrastructure and security systems division

Pace Data Center – The potential data center power infrastructure vertical

Analyzing Pace Digitek through this lens allows investors to evaluate each segment based on its own growth prospects, margins, and industry valuation benchmarks, rather than applying a single EPC multiple to the entire business.

1) SPVs under TransGreenX Energy (BOO Platform):

TransGreenX Energy currently has a BOO order book of around ₹5,025 crore. Based on my research, such assets are typically valued between 1.3× to 1.8× their asset value, especially when the project generates stable, long-term cash flows. Management has indicated that these BOO projects are expected to generate an equity IRR of around 14%. Considering that the yield on a 10-year government bond in India is roughly 6.5%, long-term institutional investors such as pension funds would generally be comfortable with a ~10% return with moderate risk. On that basis, investors might theoretically value the asset platform at around 1.5× the asset value, which would imply roughly ₹7,500 crore on a ₹5,000 crore project base. However, this approach requires adjustment.

The reason is that these projects receive approximately 30% Viability Gap Funding (VGF) from the government. For a ₹5,000 crore BOO project, this means about ₹1,500 crore comes as VGF, reducing the developer’s effective capital requirement to ₹3,500 crore. Typically, the capital structure for such infrastructure projects involves around 70% debt and 30% equity. Therefore, the adjusted project asset size attributable to the developer becomes ₹3,500 crore rather than ₹5,000 crore. Applying a 1.5× asset multiple to ₹3,500 crore gives an enterprise value of around ₹5,250 crore (enterprise value meaning market cap plus debt).

To estimate the equity value, we need to subtract the project debt. If 70% of the ₹3,500 crore capital is funded through debt, that would amount to roughly ₹2,450 crore of debt. The implied equity value would therefore be ₹5,250 crore minus ₹2,450 crore, which equals about ₹2,800 crore. However, this number may still be on the optimistic side, so it is useful to cross-check using a different valuation method.

Under the project financing structure, the developer contributes roughly ₹1,050 crore of equity (since ₹3,500 crore total cost minus ₹2,450 crore debt equals ₹1,050 crore equity). Management has indicated that the BOO projects could generate around 14% equity IRR after accounting for all costs including O&M. This would translate into roughly ₹147 crore annual return on the equity invested. If an investor is satisfied with a 10% yield, they might value this cash flow stream at approximately ₹1,470 crore.

Additionally, at the end of the project life there will still be a residual asset value. In infrastructure projects, a residual value of around 10% of asset cost is commonly assumed. Adding roughly ₹500 crore of residual value brings the valuation to about ₹1,970 crore. Based on my checks, even after 12 years of operation, BESS cells may retain around 40–45% of their capacity, so assuming only a 10% residual value does not appear aggressive.Secondly , there is option to extension with new rate.

Based on these approaches, the intrinsic value of the TransGreenX BOO platform likely falls in the range of ₹2,000–₹2,400 crore. To remain conservative, I assume a valuation of ₹2,000 crore.

Therefore, the estimated valuation for this SPV platform is around ₹2,000 crore, assuming the company can fund the ₹1,050 crore equity requirement through internal accruals along with the recently raised capital of more than ₹800 crore. At the current share price of ₹164, the market capitalization of Pace Digitek is approximately ₹3,550 crore. This effectively implies that the market is assigning a value of only ₹1,550 crore to all the remaining businesses combined. The next question then becomes: are those businesses really worth just ₹1,550 crore, or significantly more?

TransGreenX Energy (BOO Platform) intrinsic valuation : 2000 cr .

2) EPC Business Valuation

For the next year, let us assume that the company generates total revenue of around ₹4,200 crore. From this figure, we should exclude the portion that comes purely from product sales without any EPC involvement. After adjusting for this, we can reasonably assume that the EPC-related revenue would be around ₹3,500 crore. According to management guidance, the EBITDA margin in the EPC segment ranges between 8% and 10%, so taking a midpoint assumption of 9%, the EPC division could generate roughly ₹315 crore of EBITDA.

Since the EPC business is relatively asset-light and carries low debt, a large portion of EBITDA can translate into net profit. Based on this structure, the net profit could be approximately ₹220 crore. In the current market environment, reasonably growing EPC companies are generally trading at P/E multiples between 16 and 20, even though the broader market conditions remain somewhat weak. Pace Digitek’s EPC division could potentially command a higher valuation than peers because of its strong growth prospects and its strategic positioning in the emerging BESS infrastructure ecosystem, supported by its in-house product capabilities. In a more favorable market environment, the segment could even re-rate to a P/E of around 22.

However, to remain conservative, let us assume a P/E multiple of 18. Based on this assumption, the EPC division alone could command a valuation of around ₹3,960 crore, which can be rounded to approximately ₹4,000 crore by FY27, assuming the market conditions remain stable. It is important to note that this represents an intrinsic valuation based on adjusted economic activity, because under consolidated accounting the reported revenue may appear closer to ₹3,200 crore due to the elimination of inter-company product sales.

Looking slightly further ahead, we are more interested in estimating the intrinsic value by FY28. If we assume 25% growth in FY28 over FY27, the net profit could increase from ₹220 crore to around ₹275 crore. Applying the same P/E multiple of 18, the implied valuation would be ₹275 × 18 = ₹4,950 crore.

Rounding this figure, the estimated value comes to approximately ₹5,000 crore, assuming a margin of around 9%. Naturally, the valuation may vary slightly depending on whether the margin ends up closer to 8% or 10%, but the assumption used here represents a reasonable midpoint estimate.

Estimated intrinsic value of the EPC business by FY28: approximately ₹5,000 crore.

3) Pace Lineage Power BESS Division

Pace Lineage Power BESS (First Product Division):

Before estimating the probable intrinsic value of Pace Lineage Power BESS, it is important to understand the historical background of this business. In January 2011, General Electric (GE) acquired Lineage Power Holdings for approximately $520 million. Prior to this acquisition, Lineage Power was known as Tyco Electronics Power Systems, before it was sold to a private equity firm in 2007. GE’s acquisition was aimed at strengthening its presence in high-efficiency power conversion infrastructure, particularly for data centers and telecommunications networks.

Later, in 2014, Pace Digitek (which was then operating under the name Pace Power Systems) acquired the Indian business of GE Power Electronics (Lineage Power). If Pace Digitek had not acquired this division, it is quite possible that the business would have remained within GE Vernova T&D India Ltd, which today trades at extremely high valuation multiples—around EV/EBITDA of 58.4 and P/E of 83, even in the current relatively weak stock market environment.

To

estimate the economics of the BESS product division, I used the concall

transcript summary and asked an AI tool the following question:

“How

much revenue can the company generate per GWh from the BESS product

division, and what could be the profit per GWh based on concall data?”

1. Revenue for 1 GWh (Product Only)

According to the CFO, Mr. Rajavendhan P (Page 17 of the concall), the in-house product component contributes approximately ₹70 lakh per MWh (megawatt-hour).

Since:

1 GWh = 1,000 MWh

The calculation becomes:

1,000 MWh × ₹70 lakh = ₹700 crore

This implies that the company can generate approximately ₹700 crore of revenue from the product division for every 1 GWh of BESS capacity produced.

2. Profit for 1 GWh (Product Only)

Management has indicated that the EBITDA margin for the BESS product division ranges between 13% and 15% (as mentioned in Pages 12 and 16 of the concall).

Lower bound:

₹700 crore × 13% = ₹91 crore

Upper bound:

₹700 crore × 15% = ₹105 crore

Therefore, the EBITDA generated per GWh from the product division is estimated to be between ₹91 crore and ₹105 crore.

3. Net Profit Estimate per GWh

In manufacturing businesses, typically 65–75% of EBITDA converts into net profit (PAT). Assuming a 70% conversion rate, the estimated PAT would be:

PAT ≈ 0.7 × EBITDA

This results in the following approximate outcomes:

ScenarioPAT per GWhConservative₹63 croreMid case₹69 croreHigh case₹73 crore

So broadly, the net profit could range between ₹60 crore and ₹75 crore per GWh.

Taking a midpoint estimate of ₹68 crore, a 10 GWh BESS manufacturing capacity operating at full utilization by FY28 could potentially generate around ₹680 crore of net profit.

If this business were still owned by GE Vernova T&D India Ltd, the market might have valued it at a very high multiple. Even in the current relatively weak market conditions, the market might assign a P/E multiple of around 80 to such a technology-driven power infrastructure business. Under that scenario, the valuation could theoretically reach:

₹680 crore × 80 = ₹54,400 crore

However, in reality this business is no longer owned by GE, and GE has gradually moved away from the component-level DC power infrastructure business after divesting this division to Pace Digitek.

If we assume that Pace Digitek’s BESS product division achieves ₹680 crore net profit, and the market assigns a P/E multiple of only 40—which is roughly half of what GE-related companies receive—the valuation would still reach:

₹680 × 40 = ₹27,200 crore

Even this appears somewhat optimistic. To remain conservative, let us assume a P/E multiple of 30, which would imply a market capitalization of:

₹680 × 30 = ₹20,400 crore

Rounding this figure, the probable intrinsic valuation of the Pace Lineage Power BESS division could be around ₹20,000 crore by FY28. It may possible they are not able to utilize 10GW BESS plant fully or they expand to 15GW or more by FY28 . Both things possible.

Pace Lineage Power BESS (First Product Division) FY28 internsic valution = 20000 cr

4) Pace Lineage Telecom (Second Product Division):

This telecom product manufacturing division has generated significant revenue over the last two years, largely due to the large telecom equipment orders received from BSNL. These orders contributed meaningfully to the company’s recent growth in the telecom power infrastructure segment. However, at present I do not observe many new EPC contracts emerging from the telecom sector, although the company continues to receive a few standalone product orders within the telecom domain.

Given this situation, it would be prudent to take a conservative approach while estimating the future profitability of this division. Let us assume that by FY28 this telecom product segment is able to generate around ₹70 crore in net profit (PAT). Because the visibility of future telecom orders is somewhat uncertain, the market may not assign a very high valuation multiple to this business.

Instead of using a higher technology or manufacturing multiple such as P/E of 30, it would be reasonable to assume that the market values this segment at a more modest P/E multiple of around 22, reflecting the uncertainty and cyclicality of telecom infrastructure spending.

Based on this assumption, the probable intrinsic valuation of the Pace Lineage Telecom division can be estimated as:

₹70 crore × 22 = ₹1,540 crore

Therefore, the estimated intrinsic value of the Pace Lineage Telecom (Second Product Division) is approximately ₹1,540 crore.

5) Pace Defense & Aerospace

This is a new division that the company is beginning to develop. At this stage it is difficult to estimate how the market might value this segment, but the opportunity itself appears quite significant for Pace Digitek. The company’s existing technical capabilities—particularly its 48V DC power systems, modular BESS (Battery Energy Storage Systems), and the legacy technology inherited from the Lineage Power platform—place it in a strong position to address several critical power and energy challenges emerging within the defense and aerospace sectors.

Modern defense infrastructure increasingly depends on reliable, modular, and high-efficiency power systems, and this is precisely where Pace Digitek’s technological strengths lie. Their expertise in power electronics, DC power architecture, and energy storage integration could enable them to participate in multiple areas within the defense and aerospace ecosystem.

Below is a simplified breakdown of how their products and capabilities could fit into the broader value chain of defense and aerospace power infrastructure:

1. Military Microgrids & Forward Operating Bases (FOBs)

In modern warfare, power is a logistical bottleneck. Pace Digitek’s containerized BESS can replace or hybridize traditional diesel generators.

Tactical Advantage: BESS allows for “Silent Watch” capabilities—powering communications, surveillance, and cooling without the thermal and acoustic signature of a diesel engine, making bases harder to detect by enemy thermal sensors.

Value Chain Role: Primary Power Infrastructure. Their IP-55 rated outdoor cabinets are ideal for rugged, dusty, or extreme temperature environments typical of military deployments.

2. Directed Energy Weapons (DEW) Support

The defense industry is moving toward Laser and High-Power Microwave (HPM) weapons. These systems require “Pulse Power”—the ability to discharge massive amounts of energy in milliseconds.

The 48V Advantage: Pace’s 48V DC rectifiers and high-discharge lithium-ion battery packs (like the 314AH packs supplied to Reliance) can provide the stable, high-current DC backbone required to “charge” the capacitors of directed energy weapons.

Value Chain Role: Sub-system Power Supply.

3. Aerospace Ground Support Equipment (GSE)

The aerospace industry is aggressively pursuing “Green Airports” and electric ground operations.

Electric Tug & Loader Charging: Airports are transitioning from gas-powered tugs to electric. Pace’s BESS can act as a buffer, storing solar energy during the day to fast-charge ground support vehicles at night without overloading the airport’s main grid.

Pre-Conditioned Air (PCA) & Start-up Power: Their 48V DC systems find a place in powering the sensitive avionics of aircraft while they are parked at the gate (Ground Power Units), ensuring “clean” power that doesn’t damage expensive flight computers.

Value Chain Role: Airport Infrastructure & Ground Support.

4. RADAR and Communication Hardening

Defense communication networks (SATCOM hubs and RADAR installations) require absolute uptime and “clean” DC power.

Legacy Lineage Power IP: Radars operate on DC power. Pace’s high-efficiency rectifiers (like the LP4000 series) convert AC utility power to stable DC with over 96% efficiency.

EMP Shielding Potential: As Pace manufactures its own containers and cabinets, they have the capability to integrate Faraday cage-style shielding (EMI/EMC protection) into their power units, which is a mandatory requirement for defense-grade power systems.

Value Chain Role: Critical Mission Infrastructure.

5. Naval & Marine Power Management

Modern naval vessels are essentially “floating microgrids” with an increasing number of DC loads (electric propulsion, sensors, and electromagnetic railguns).

Modular Storage: Pace’s modular BESS can be used for “peak-shaving” on ships, allowing engines to run at optimal RPMs while the batteries handle the sudden surges in power demand from sensors or weapons systems.

Value Chain Role: On-board Power Distribution.

6. Unmanned Aerial Vehicle (UAV) Ground Control Stations

As India ramps up its drone capabilities (UAVs), the Ground Control Stations (GCS) and data links require portable, ruggedized power.

Mobile Power Units: Pace can provide trailer-mounted BESS units that power the command-and-control centers for drone swarms in remote border areas where the grid is non-existent.

Strategic Positioning for Pace Digitek

To fully capture this value chain, Pace Digitek would likely leverage two specific Indian government initiatives:

iDEX (Innovations for Defence Excellence): Utilizing their BESS technology to solve the “last-mile power” challenge for the Indian Army in high-altitude regions (e.g., Ladakh).

Make in India (Aatmanirbhar Bharat): Since Pace owns the IP and manufacturing for the cells-to-container process, they qualify as a Class-1 local supplier, giving them a significant advantage over global competitors like Schneider or Delta in Indian defense tenders.

Significant opportunity for pace digitek in defence and aerospace . But , benefits of doubt just give valuation of just 800 cr for FY28

Standalone defence and aerospace business intrinsic value ( FY28) = 800cr.

6) Pace ICT

Pace Digitek has recently secured an order worth around ₹90 crore from RailTel Corporation of India Ltd. This order relates to high-fidelity monitoring systems that comply with the latest RDSO/SPN/TC/106/2025 Version 3.1 specifications. Only a very limited number of Indian companies have been able to qualify under this updated specification listed space Pace Digitek and L&T. Based on my understanding, foreign players are generally not permitted to participate directly in this category, which further strengthens the competitive position of qualified domestic companies.

Obtaining approval under Version 3.1 is considered both technically demanding and operationally complex. It is not a simple “off-the-shelf” certification process. Instead, it requires companies to satisfy multiple layers of rigorous technical standards, testing protocols, and regulatory approvals before they are eligible to participate in such projects.

Meeting these requirements involves clearing several stringent approval stages, which makes the qualification process both time-consuming and technically challenging.

STQC Approval: OEMs must possess STQC (Standardisation Testing and Quality Certification) approval for both the cameras and the Mobile Network Video Recorder (MNVR) software before the tender opening date. This is a high-bar security clearance from the Ministry of Electronics & IT.

Rigorous Testing (RDSO Spec): The Version 3.1 update (dated June 2025) introduced stricter requirements for high-fidelity monitoring, H.265 compression, and real-time LTE/Wi-Fi accessibility. Equipment must be “proven” and able to withstand the vibration, dust, and electrical surges of a moving train (Rolling Stock environment).

Backward Integration & Maintenance: Tenders often demand a 3-year warranty followed by a 5-year Comprehensive Annual Maintenance Contract (CAMC). This means companies must have a robust service network across India, which is a barrier for smaller or newer players.

System Integration Complexity: The specification requires the system to be based on a non-proprietary open architecture. This means the hardware must be able to integrate with any software/IT hardware via shared SDKs, requiring significant engineering flexibility.

Security infrastructure projects in the railway sector represent only one segment of a much larger opportunity. Similar monitoring and security systems are required across several other domains such as airports, data centers, and other national critical infrastructure including ports, refineries, and strategic facilities.

Therefore, the long-term potential for this division could be substantial. However, at present the business is still in its early stages of development. Because projects in this segment involve stringent regulatory standards, high technical requirements, and complex system integration, companies operating in this space can eventually achieve relatively strong profit margins, potentially reaching around 18-20% over time.

For the purpose of valuation, let us take a conservative assumption and estimate that this division could generate around ₹70 crore in net profit (PAT) by FY28. If the market assigns a P/E multiple of 30 to such a technology-driven infrastructure business, it would provide a reasonable basis for estimating its potential valuation.

Standalone Pace ICT business intrinsic value ( FY28) = 2100cr.

7) Pace Data Center:

Management has not specifically mentioned the data center segment in either the investor presentation or the recent concall. However, based on my analysis, the company appears to possess meaningful capabilities in data center power systems. Many of their existing products—particularly those related to power electronics, DC power architecture, and energy management—are closely aligned with the requirements of modern data center infrastructure.

That said, the company would likely need some additional R&D investment or a strategic technology partnership to seriously build out a dedicated data center division. At present, Pace Digitek is already active across multiple business verticals, and as a result management may not yet be focusing heavily on the data center opportunity.

Nevertheless, the data center power infrastructure market is expanding rapidly, and this opportunity is effectively knocking on the company’s door. Given their existing expertise in power systems and energy storage, they could potentially enter this space without starting from scratch.

Interestingly, if one visits the company’s website (https://lineagepowersystems.com), Data Center is already listed as one of the business verticals. However, to be realistic, the company has not yet demonstrated a strong strategic focus on capturing data center opportunities so far.

Acquisition of Lineage Power: In January 2011, General Electric (GE) acquired Lineage Power Holdings for approximately $520 million.

Lineage Power was formerly known as Tyco Electronics Power Systems before being sold to a private equity firm in 2007.

This acquisition allowed GE to expand its footprint in high-efficiency power conversion infrastructure for data centres and telecommunications.

When Pace Digitek (then known as Pace Power Systems) acquired the Indian business of GE Power Electronics (Lineage Power) in 2014, the primary focus was on the telecommunications sector even though Lineage Power had some capabilities of data center in 2014 . They might have not worked on upgrading data center capabilities but their telecom , BESS power management and up to some extent cooling capabilities find place in data center . They may need to tweak it or tie up with someone .

In 2026, a Battery Energy Storage System (BESS) is no longer just an “extra”—it is becoming a strategic requirement for modern, large-scale data centers.

While every data center has always required an Uninterruptible Power Supply (UPS) for short-term backup, a BESS represents an evolution that handles more than just power outages.

Why BESS is becoming a Requirement in Data Center

1. Managing Volatile AI Workloads

AI-heavy data centers (using high-density GPUs) experience massive “swings” in power demand. Traditional power grids and older UPS systems often struggle with these sudden spikes. A BESS acts as a buffer, discharging rapidly to cover those surges and protecting the grid from instability.

2. Peak Shaving (Cost Control)

Electricity providers often charge “demand charges” based on a facility’s highest peak usage.

The BESS Role: It charges during low-cost, off-peak hours and discharges during peak times. This “shaves” the peak off the facility’s grid demand, potentially saving 20%–30% on monthly energy bills.

3. Replacing Diesel Generators (ESG Goals)

With strict 2026 sustainability regulations (like the EU’s Energy Efficiency Directive and similar Indian ESG mandates), data centers are under pressure to reduce Scope 1 emissions. BESS can bridge power gaps for hours instead of minutes, allowing facilities to significantly reduce or eventually eliminate the testing and use of carbon-heavy diesel generators.

4. Grid-Interactive Revenue

Modern data centers are now “prosumers” (producers + consumers). By using a BESS, a data center can participate in Frequency Regulation—selling energy back to the local grid to help stabilize it. This turns the power infrastructure from a “cost center” into a “revenue generator.”

The power grid must maintain a very specific frequency (e.g., 50Hz in India or 60Hz in the US) to remain stable. If demand suddenly spikes or a power plant goes offline, the frequency drops; if there is too much power, it rises.

BESS as a Stabilizer: A BESS can respond in milliseconds—much faster than a traditional power plant.

The Service: When the grid frequency fluctuates, the data center’s BESS either absorbs excess energy or injects stored energy to balance the grid.

The Reward: Utilities pay data center operators “ancillary service” fees for providing this stabilization, as it prevents blackouts and reduces the need for expensive “peaker” power plants.

The transition from standard AC (Alternating Current) power to 48V DC (Direct Current) architectures—a domain where Pace Digitek’s Lineage Power excels—is a fundamental shift driven by the extreme power density of AI workloads.

By leveraging the legacy GE “Lineage” IP, Pace Digitek provides a 48V ecosystem that bypasses the inefficiencies of traditional data center power chains.

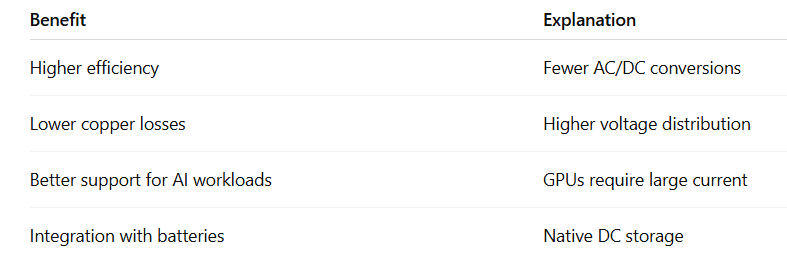

The Efficiency Physics: Why 48V Wins

The primary driver for Pace’s 48V architecture is the rreduction in $I^2R$ (resistive) losses..

The Math: Power loss in a cable is proportional to the square of the current ($I$). In modern AI racks requiring 100kW+, a 12V system would require massive cables. By using 48V, the current is reduced by 4x, which reduces the heat loss by 16 times ($4^2$).

Conversion Efficiency: Standard AC systems convert power back and forth between AC and DC multiple times. Each “hop” loses 2–3% energy. Pace’s LP4000V48-T1 rectifiers convert AC utility power directly to 48V DC with >96% efficiency, delivering power straight to the battery and the load without further inversion.

2. Material and Copper Savings

As Pace manufactures its own IP-55 cabinets and racks, they capitalize on the reduced material needs of 48V systems:

Copper Reduction: Because the current is lower, 48V DC systems require significantly thinner copper busbars. Industry data suggests 48V racks can use up to 80% less copper than 12V equivalents.

Cost Advantage: For a hyperscale facility, this translates into millions of dollars in raw material savings, which helps Pace maintain competitive pricing against global giants.

3. Product Spotlight: Lineage Power’s Edge

Pace Digitek’s recent Rs. 158.71 Crore order from Reliance Industries (February 2026) for 48V 314AH battery packs highlights their specific technological sweet spot:

The Rectifier (LP4000V48-T1): This is the “brain” of their system. It is a hot-pluggable, fan-cooled module capable of 20,000W constant output. It handles wide voltage fluctuations (common in India) and communicates via CAN bus for real-time monitoring—essential for AI data centers that cannot afford a millisecond of downtime.

Modular Redundancy: Unlike a single large AC UPS which is a “single point of failure,” Pace’s 48V systems are modular. If one rectifier module fails, the others in the rack take over without interruption ($N+1$ redundancy).

4. Integration with Renewables

Data centers are under pressure to be “Green.”

Solar panels and BESS units (Pace’s core strength) naturally produce DC power.

In an AC data center, solar energy must be converted to AC, then back to DC for the servers.

In Pace’s 48V DC ecosystem, the solar/battery power stays in DC form, eliminating the “Inverter stage” entirely and boosting renewable utilization efficiency by ~10%.

Why This Matters for Companies Like Pace Digitek

Pace Digitek’s capabilities include:

48V DC power systems

Rectifiers

Battery energy storage (BESS)

DC power infrastructure from Lineage Power

These technologies are directly relevant to modern data center DC architectures, where companies like Vertiv, Delta, and Huawei Digital Power dominate today.

The "Lineage" Legacy Advantage: Because they own the legacy GE Power Electronics (Lineage) IP in India, they already have the "blueprints" for the power conversion modules (rectifiers/converters) that are standard in global data center racks.

GE Vernova vs Pace Digitek

The relationship between Pace Digitek (through its subsidiary Lineage Power) and GE Vernova is rooted in a 2014 acquisition, but today they operate at different layers of the data center and energy value chain.

If Pace Digitek enters the data center (DC) market, they are more likely to be complementary partners or tier-2 suppliers rather than direct competitors to GE Vernova in the high-voltage/grid space.

1. The Legacy Connection

In 2014, Pace Digitek (then Pace Power Systems) acquired the GE Power Electronics India business. This deal gave Pace the rights to use the Lineage Power brand in certain regions and sectors (primarily India and telecom).

GE’s Path: GE eventually moved away from the component-level DC power business. The global Lineage Power business (GE Critical Power) was sold to ABB in 2018. The remaining energy businesses of GE were recently spun off into GE Vernova.

Pace’s Path: Pace has used the Lineage brand to build a powerhouse in DC power systems and BESS (Battery Energy Storage Systems), focusing on the “back-of-the-meter” infrastructure.

2. Value Chain Comparison: Who Does What?

In a data center project, the power management requirements are split into different “layers.” Here is how they differ:

If Pace Digitek enters the Data Center market, their primary competitors will be companies like Delta Electronics, Vertiv, or Schneider Electric, who compete in the "rack-to-battery" space. GE Vernova is positioned much "higher" in the chain, dealing with the utility grid and massive power plants.

3. GE Vernova vs Pace Digitek Are Competing?

While there is a slight overlap in BESS (Battery Energy Storage), their “Power Management Systems” serve different masters:

No Direct Competition in DC Core: GE Vernova does not typically manufacture the 48V DC battery modules or telecom-style racks that Lineage Power specializes in. GE Vernova is “Heavy Electricals,” whereas Pace/Lineage is “Power Electronics.”

Complementary Nature: In a modern AI data center, GE Vernova might build the substation that brings 110kV power to the site, while Pace Digitek would provide the containerized BESS that sits next to the building to handle peak-shaving or emergency backup for the servers.

The “Lineage” Brand: Since Pace owns the brand rights for the legacy DC products in India, they occupy a niche that GE Vernova has largely exited.

Summary

If Pace Digitek enters the Data Center market, their primary competitors will be companies like Delta Electronics, Vertiv, or Schneider Electric, who compete in the “rack-to-battery” space. GE Vernova is positioned much “higher” in the chain, dealing with the utility grid and massive power plants.

Since this division is not started yet I am giving hope valution of 11 cr .

Conclusion: Intrinsic Valuation Framework

Based on the above assumptions, the following could represent potential intrinsic values of Pace Digitek’s divisions.

Total Potential Internsic Valuation: 31500 cr .

It offers huge margin of safety from current 3500 cr Valuation for 2 years horizon.If we are wrong by 50% still it can create significant value .

Current Issues and My View

High Debt:

The company is expected to carry around ₹2,500 crore of debt on its books, but this debt will primarily sit within the SPVs under TransGreenX Energy (the BOO platform) rather than on the operating businesses. The other divisions—such as EPC, product manufacturing, and telecom—are likely to maintain relatively low or manageable levels of debt. Management has also indicated that they may either list this BOO platform separately or monetize it through asset sales in the future. Therefore, in my view, the presence of this debt should not be considered a major concern for the core operating businesses.

2. High Receivables:

At present, the company has trade receivables of roughly ₹1,800 crore, largely due to the large BSNL telecom project related to tower erection. According to management commentary, this project is now approaching completion and the final milestones are being achieved.

As these milestones are closed and billed, the outstanding receivables

should begin converting into cash. Based on this timeline, the

receivable position is expected to improve significantly by September 2026, which should help normalize the company’s working capital cycle.

Unbilled means invoice generated but due date in future .

Not Due means invoice is also not generated yet , It means there is some time gap between booking revenue in account system and generating invoice as per term of contract. Around 120 cr amount is greater than 1 year that is risk.

If you look only trade receivables then figure looks worrisome but when you look complete picture including Inventory Days,Receivable Days,Payable Days and Cash Conversion Cycle then it looks amazingly good manage company . in fact it has better Cash Conversion Cycle than FMCG companies like HUL . Not sure how they are able to do it . Payable days of of 459 days is unbelievable . Because of this their debt level is low

Pace Digitek

HUL

In many cases, companies that work extensively with government-owned clients such as BSNL tend to experience higher receivable cycles, as payment timelines in such projects are often linked to milestone approvals and administrative processes. Pace Digitek has faced a similar situation in the past. However, the company has recently expanded its customer base to include several large private-sector clients, such as L&T, Reliance, Bondada, and Advait Energy. Payments from such clients are generally expected to be faster and more predictable compared to traditional government contracts.

In addition, the company’s BOO structure through SPVs under TransGreenX Energy is also likely to help improve cash flow visibility. Since these SPVs are financed through structured project funding, payments to the EPC contractor can occur relatively quickly once project milestones are achieved. While the company will continue to undertake some pure EPC contracts with government entities, the overall receivable cycle is expected to improve significantly over the next 12 months as the mix of clients shifts and the BOO platform begins to contribute more meaningfully.

The company is currently facing some issues with receivables, but overall its working capital position remains strong, which is what matters most.

Government Regulation: 20% Localization Requirement in BESS Containers

Why This Regulation Helps Pace Digitek

India has introduced domestic content requirements (DCR) in several Battery Energy Storage System (BESS) tenders, especially those issued by government agencies such as SECI (Solar Energy Corporation of India) and supported through schemes like Viability Gap Funding (VGF). One of the key provisions in these tenders is the requirement that a minimum portion of the BESS system must be manufactured or assembled within India. In many projects, this requirement is around 20% localization for the containerized BESS system.

The localization requirement creates a significant structural advantage for companies that already manufacture BESS systems domestically.

Pace Digitek is one of the few companies in India that has in-house BESS system integration capability, primarily through its Lineage Power technology platform.

Their capabilities include:

DC power electronics

battery rack integration

containerized BESS systems

thermal management

power conversion infrastructure

Because of this, Pace Digitek can meet localization requirements without depending heavily on foreign integrators.

The market is currently grouping all BESS players under a single umbrella, but that is not accurate. In reality, there are four distinct types of BESS players.

Annuity income seekers – These players primarily have capital and aim to earn a 12–15% yield. They typically lack deep sector knowledge and do not own BESS battery container manufacturing facilities, so they outsource execution to EPC contractors once the won BESS BOO tender bid. e.g. Patanjali , Sunsure Energy

Pure EPC players – Companies that specialize only in engineering, procurement, and construction of BESS projects but do not manufacture core components. e.g. Power Mech

EPC players with BESS battery container manufacturing – Firms that not only execute projects but also manufacture BESS battery containers, giving them greater control over the value chain. e.g. Advait

Players with BESS power management system capabilities – Companies that possess advanced power management system (PMS) capabilities, enabling them to manage and optimize battery performance and grid integration. e.g. Pace Digitek .

We can see that Pace Digitek is present across the entire value chain, and to some extent Servotech may also have a similar positioning. (I have not conducted deep research on all the players mentioned—these are only illustrative examples, and they may possess additional capabilities beyond what is stated.)

Why the Data Center Opportunity Is a Natural Extension of Pace Digitek’s BESS Capabilities ?

Lineage Power historically specialized in DC power infrastructure, particularly for telecom networks and mission-critical facilities. This expertise could become increasingly valuable as data center power architecture evolves.

The Traditional Data Center Power Architecture

Most legacy data centers were designed around AC power distribution.

Although servers ultimately run on DC power, electricity undergoes multiple AC/DC conversions before reaching the hardware.

These conversions introduce:

energy losses

heat generation

additional hardware complexity

Efficiency losses can reach 15–20% in some architectures.

Large hyperscale data center operators are gradually exploring direct DC power distribution, particularly in combination with:

renewable energy

battery storage

AI computing clusters

In a DC architecture, the power path can become significantly simpler:

48V DC Is Becoming Important

Many next-generation data center designs are moving toward 48-volt DC rack power systems.

Advantages include:

Pace Digitek’s inherited Lineage Power technology stack includes:

high-efficiency DC rectifiers

48V DC power systems

telecom power infrastructure

battery integration

Telecom networks historically relied on 48V DC architecture, which is remarkably similar to what modern data centers are beginning to adopt.

Companies like Meta, Google, and Microsoft have already experimented with 48V DC rack architectures.

Major technology firms (Hyperscalers) and specialized data center operators have already begun replacing traditional diesel backup with Battery Energy Storage Systems (BESS). This shift is driven by the need for faster response times, grid stability, and sustainability goals.

The following data centers and operators have publicly implemented or announced BESS projects:

1. Google

Location: Pine Island, Minnesota, US.

Project: In March 2026, Google announced a partnership with Xcel Energy to deploy a 300 MW / 30 GWh iron-air battery—the world’s largest.

Purpose: Unlike traditional lithium-ion batteries that provide 4 hours of backup, this “iron-air” technology (by Form Energy) provides 100 hours of long-duration storage, handling multi-day intermittent renewable power.

Belgium: Google also operates a data center in Belgium that utilizes solar power paired with battery storage.

2. Microsoft

Location: Stackbo, Sweden.

Project: Microsoft replaced conventional diesel generators with Saft’s MW-scale lithium-ion BESS.

Performance: The system acts as a grid-forming microgrid with black-start capability, providing 80 minutes of autonomous power during outages.

Dublin, Ireland: Nearing completion in late 2025/early 2026, Microsoft is using batteries instead of diesel generators for “grid-interactive UPS,” which allows the data center to sell power back to the grid when not needed.

Australia: In Melbourne, Microsoft used BESS solutions (provided by Ampd Energy) during the construction phase of their data centers to reduce diesel usage by 74%.

3. Pure Data Centres (Pure DC)

Location: Dublin, Ireland.

Project: In March 2026, Pure DC launched Europe’s first large-scale 110 MW on-site microgrid.

Purpose: The microgrid uses BESS to manage load fluctuations and resilience before a full connection to the national grid is established, supporting early-phase operational AI infrastructure.

4. Amazon (AWS)

Implementation: Amazon has integrated BESS into its global infrastructure strategy to meet its goal of 100% renewable energy.

Function: AWS uses BESS to collect solar/wind energy during off-peak hours (like at night) and discharge it during peak demand. They also use Battery Digital Twins on AWS to monitor real-time health (voltage/temperature) of their storage systems.

5. Apple

Location: Reno, Nevada, US.

Project: Apple’s Nevada data center is supported by a large on-site battery bank.

Outcome: This allows the facility to run on 80% solar energy, as the batteries store daytime solar production and discharge it during the night.

Data centers in the APAC region (Google Singapore, NTT Japan, Equinix Australia) are currently focused on 1–4 hour lithium-ion systems for grid services and peak shaving. True 8–100 hour storage is still in the pilot or early deployment phase, primarily in the United States and Europe.

Conclusion:

The market opportunity for Pace Digitek appears to be significantly large, supported by a capable management team and expanding business verticals. While concerns such as high receivables

currently exist, they appear to be manageable and potentially

temporary. At the same time, the company trades at what seems to be an attractive valuation, partly due to the accounting-related optical illusion that understates its underlying economic activity. It will be interesting to see when and how the market begins to recognize the company’s true potential.

My Conviction Level: 9 / 10

Valuation Margin of Safety: Very high (current market capitalization around ₹3,500 crore)

Portfolio Allocation Comfort: 12–15%, even though I maintain a diversified portfolio

Time Spent on Research: 18+ hours (I even took one day off from my full-time IT job to work on this analysis)

This article should be treated only as a starting point for your own research and analysis.

And if you happen to make decent returns over the next three years, don’t forget to send a coffee or a box of mithai as a small token of appreciation. But,it doesn’t turn around as expected then “bhai samajke maph kar dena” .

No comments:

Post a Comment